Background Information about the Inflation Reduction Act and Biogas Projects.

In August 2022, the Inflation Reduction Act (IRA) was signed into law. A significant portion of this new legislation is designed to increase the production of clean energy and reduce carbon emissions. In addition to renewable energy technologies, such as solar and wind, the legislation has expanded its list of qualified technologies to receive extensive tax credits also to include Biogas Systems.

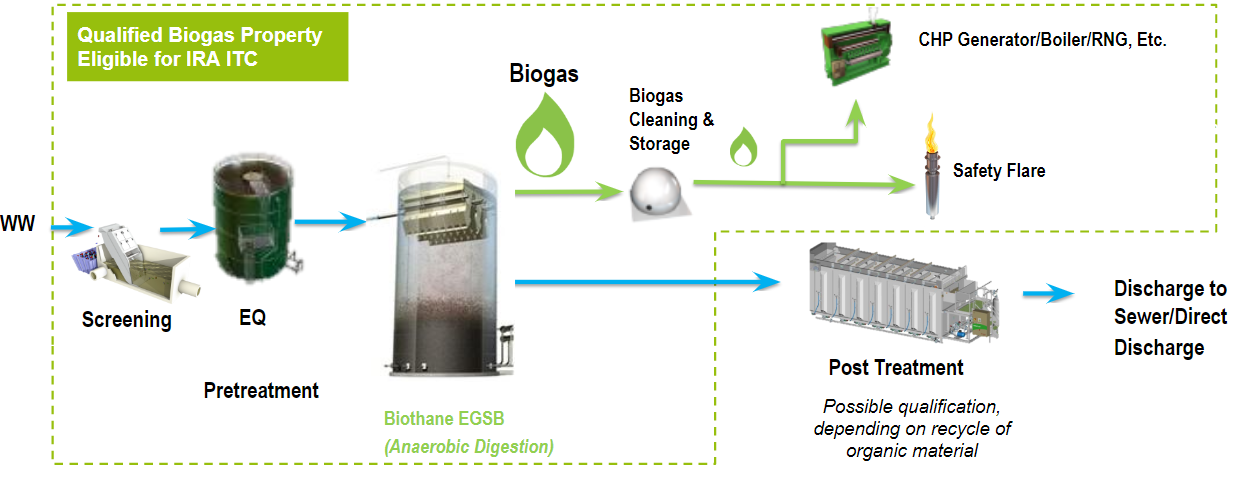

As a result, an entity that installs an anaerobic digestion system to treat wastewater and productively uses the biogas can significantly offset its CAPEX investment through the investment tax credits (ITC) offered through the Inflation Reduction Act (IRA).

Download the Investment Tax Credits Information Guide for Anaerobic Digestion & Biogas Projects

Key Facts about Biogas Projects from Anaerobic Digestion and Investment Tax Credit Benefits

Potential Savings

All projects will qualify to receive a minimum tax credit of 6%. However, most projects will likely qualify for 30% tax credit if it meets specific criteria. There is also the potential for additional tax credit bonuses, such as using domestic content and installing a system in a certain qualifying geographic area. These bonuses can boost savings by up to 50%.

What equipment can qualify for Investment Tax Credits under the Inflation Reduction Act?

Equipment that is required for the transformation of biomass into gas will likely qualify for investment tax credits within the scope of the Inflation Reduction Act. This includes the anaerobic digestion systems that treat wastewater. In addition to the reactor, related pretreatment technologies and any other tertiary equipment needed to clean and use the gas qualify for the ITC.

What if I already have an anaerobic digestion system?

If you have an existing anaerobic treatment system and are not collecting and using your biogas (for instance if you are flaring your biogas), you can retrofit your anaerobic digestion system with biogas cleaning, handling, and utilization equipment. This investment will likely qualify for the investment tax credit.

What is the timeline for a biogas project to qualify for the Inflation Reduction Act Tax Credits?

Projects that are commissioned after December 31, 2022, or start construction prior to December 31, 2024, can qualify for investment tax credits.

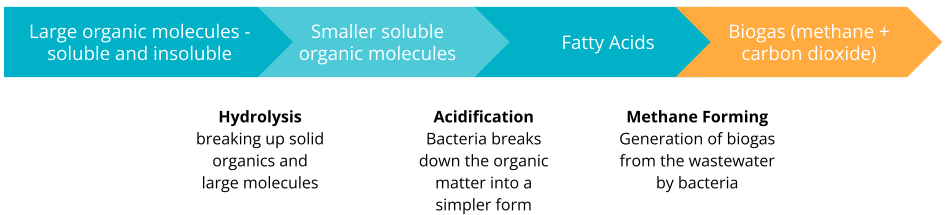

What is Anaerobic Digestion & How Does it Work?

During anaerobic treatment, bacteria transform organic waste into energy in the complete absence of oxygen. This transformation is naturally occurring and commonly used to treat the wastewater from both municipal and industrial sources.

A natural by-product of this biological process is methane (biogas). This biogas can be extracted from the reactor, cleaned, and utilized as an on-site energy source. Anaerobic treatment technologies, such as the Biobed® Advanced, is a patented technology that allows for enhanced digestion of dissolved organics in wastewater streams.

Basic Anaerobic Digestion Process

Need help navigating the best option for your wastewater or biogas project?

Our experts are able to help you explore the available technologies and evaluate the best option for your facility.

Definitions and More Detailed Information Regarding the Inflation Reduction Act

About the Inflation Reduction Act of 2022

On August 16, 2022, President Biden signed into law the Inflation Reduction Act of 2022 (the Act), which extends and expands existing tax credits and adds several new energy tax credits to encourage the production of clean energy and reduce carbon emissions. Section 48(a) of the Internal Revenue Code (IRC) as it existed prior to the adoption of the Act provides an investment tax credit (ITC) for the installation of certain renewable energy property as described in Section 48(a)(3). The Act amended Section 48(a)(3) to include additional categories of energy property, one of which is “qualified biogas property.”

What is a “Qualified Biogas Property”?

According to the legislation, a “qualified biogas property” is defined as property comprising a system that converts biomass into a gas which (A) consists of not less than 52% methane by volume or (B) is concentrated by such system into a gas which consists of not less than 52% methane, and (ii) captures such gas for sale or productive use and not for disposal via combustion. Qualified biogas property is defined to also include any property which is part of such system which cleans or conditions such gas.

Increases to Base Investment Tax Credit (ITC)

The base rate for a biogas project is 6%. A taxpayer with a qualified biogas property project is eligible to increase the ITC rate from a six percent base rate to up to 30% if (i) its project’s maximum net output is less than one megawatt of electrical or thermal energy, (ii) its project begins construction prior to the 60th day following the Secretary of the Treasury’s publication of guidance on the prevailing wage and apprenticeship requirements, or (iii) it satisfies prevailing wage and apprenticeship requirements. A taxpayer may also receive an additional 10% domestic content bonus credit amount and a 10% energy community bonus credit amount, thereby potentially increasing the ITC rate to 50%.

Domestic Content Bonus Credit

A taxpayer is eligible to receive an additional 10% domestic content bonus credit amount if it satisfies the Project Requirements, and it certifies to the Secretary (at such time, and in such form and manner, as the Secretary may prescribe) that any steel, iron, or manufactured product which is a component of such facility (upon completion of construction) was produced in the United States. As it relates to manufactured products which are components of the facility upon completion of construction, such products will be deemed to have been produced in the United States if not less than 40% (20% for offshore wind facilities) of the total costs of all such manufactured products of such facility are attributable to manufactured products (including components) which are mined, produced or manufactured in the United States. If a taxpayer’s project does not meet the Project Requirements but otherwise satisfies the domestic content requirements, then the taxpayer is eligible to receive a two percent domestic content bonus credit.

Energy Community Bonus Credit

A taxpayer is eligible to receive an additional 10% energy community bonus credit amount if it satisfies the Project Requirements, and the project is placed in service within an energy community. An energy community is defined as (i) a brownfield site, (ii) a metropolitan statistical area or non-metropolitan area which (A) has (or, at any time during the period beginning after December 31, 2009, had) 0.17% or greater direct employment or 25% or greater local tax revenues related to the extraction, processing, transport, or storage of coal, oil, or natural gas (as determined by the Secretary), and (B) has an unemployment rate at or above the national average unemployment rate for the previous year (as determined by the Secretary), or (iii) a census tract (A) in which (y) after December 31, 1999, a coal mine has closed, or (z) after December 31, 2009, a coal-fired electric generating unit has been retired, or (B) which is directly adjoining to any of the forgoing census tracts. If a taxpayer’s project does not meet the Project Requirements but otherwise satisfies the energy community requirements, then the taxpayer is eligible to receive a two percent energy community bonus credit.

Need more info? click here to read the entire Inflation Reduction Act of 2022

The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought.