Water-solubles: rising star of the specialty market

As the rising star in the fast-growing specialty plant nutrients market, smart fertilizer producers are expanding their water-soluble product portfolios. Sana Boulabiar and Matias Navarro, Veolia Water Technologies North America, explain the attraction.

Specialty products for specialty crops

Two agricultural sector trends link together the popularity of specialty fertilizers with specialty crops. Firstly, growing interest in healthy eating and rising disposable incomes are driving up the consumption of fresh fruits and vegetables, leading to an expansion in horticulture devoted to specialty crops. Secondly, these intensively-cultivated and sensitive crop types are also increasingly grown using micro-irrigation or hydroponic systems, often within greenhouses.

Both trends are boosting demand for highly-soluble products that can be injected into irrigation or hydroponic systems to directly supply fruit and vegetables with nutrients alongside water – a practice known as fertigation.

Meanwhile, conventional fertilizers that are less soluble and more impure are increasingly falling out of favor, as the chemical impurities present can damage roots and foliage. Their insoluble content can also damage expensive micro-irrigation equipment by clogging subsurface drip lines and emitters, impairing operations and incurring significant repair costs.

Water, water everywhere – but for how long?

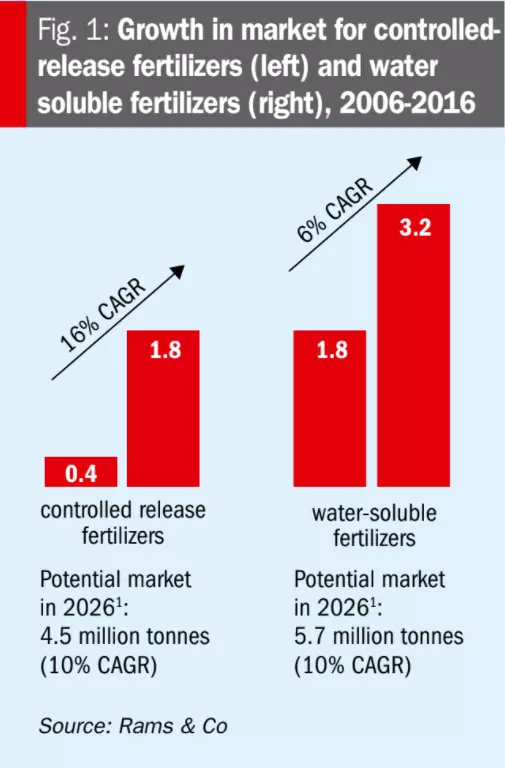

Agriculture will increasingly have to compete with other users to access water. By 2050, for example, more than half of the world’s projected population of 9.7 billion people will live in water-stressed regions, according to MIT researchers. Consequently, flood irrigated land, which represents about 37 percent and 34 percent of the total arable land in China and India, respectively, will need to undergo large-scale conversion to more water efficient systems that minimize water usage. These include modern precision agriculture methods such as micro-irrigation (drip irrigation). Such methods optimize soil moisture conditions while delivering greater efficiencies in land and water usage. Although the micro-irrigation market has traditionally been dominated by Europe, the future growth potential lies in Asia-Pacific where China and India apply drip irrigation to just 0.6 percent and two percent of their arable land, respectively. As a consequence, the adoption of water-soluble fertilizers is gaining pace (Figure 1) as growers look for higher returns. Their use is also being driven by more investment in micro-irrigation infrastructure, greater regulatory scrutiny over nutrient losses, and the growth in fertigation and foliar application. The burgeoning value of the water-soluble fertilizer market – estimated to be above $15 billion currently – means it is gaining the attention of most fertilizer majors.

Water-soluble fertilizers, the rising star

Water-soluble fertilizers exhibit a range of highly desirable properties. Their purity, efficacy as plant nutrients, overall handling properties and long-term thermal stability are all superior to other formulations.

Water-soluble fertilizers, despite their attractiveness, have generally been regarded as a niche segment of the overall market. Yet there is good evidence that this is beginning to change. Research by consultants CRU shows that, of the top 10 NPK grades currently placed on the market by fertilizer producers globally, the second and third most frequently offered types are NPK 18-18-18 and 20-20-20, respectively, both of these being water-soluble fertilizers. Similarly, CRU’s research also shows that water-soluble MAP (12-61-0) is now the second most offered NP grade worldwide. While, for PK grades, soluble MKP (0-52-34) topped the ranking as the most offered grade globally.

This authoritative analysis, being based on product data from around 50 of the world’s largest compound NPK producers, demonstrates how the growing availability of water-soluble NPK grades is challenging the dominant market position of other formulations such as NPK granules and blends.

The power of crystallization

Of all the many categories of specialty fertilizers entering the market – ranging from controlled-release and slow-release fertilizers (CRFs and SRFs) to stabilized nitrogen fertilizers (SNFs) and micronutrient products – crystalline water-soluble formulations are emerging as the hottest-selling products on the global fertilizer market due to their high performance characteristics. Being fully-soluble, highly-pure (typically >99%wt), with very low-to-zero levels of sodium, chlorine or heavy metals, and also largely free of the insoluble impurities (usually less than 0.1%wt) that can clog spray and dosing systems, they are an excellent match for the needs of modern farmers.

As a result, established crystallization processes are currently experiencing a renaissance. This is being spurred by renewed interest in reliable production technology for water-soluble fertilizers that is capable of meeting product requirements for purity and solubility. One of the main advantages of crystallization technology is its ability to consume lower-grade raw materials as feedstocks, even waste streams, and convert these into high-value fertilizer products. The ability to accept such feedstocks, without additional pre-treatment steps, delivers a huge cost saving to fertilizer producers. The reuse of low-grade or waste materials also fulfils sustainability criteria.

One powerful example of crystallization’s capabilities is the conversion of merchant grade phosphoric acid (MGA) into water-soluble phosphate products. This process can be specifically designed to achieve targets for purity, crystal shape and size to match a particular application. Crystallization technology also comes with proven production results and low process risks.

Crystallization is also an effective production process for the manufacture of high-quality water-soluble SOP (sulfate of potash). A range of different feedstocks of varying quality can be used to produce SOP crystals. Sodium sulfate brines or other natural brines, including polyhalite brines (K2SO4.2CaSO4.MgSO4.2H2O), schoenite brines (MgSO4.K2SO4.6H2O) and even kainite brines (KCl.MgSO4.3H2O), are all suitable. Another option is to manufacture SOP from the waste streams of pulp and paper mills. In this process, glaserite (a double salt of SOP and sodium sulfate) is initially recovered via a black liquor ash treatment system and then converted into high-quality SOP crystals for fertilizer use. Whatever the feedstock option, the crystallization process holds the key when it comes to controlling the purity and the size of the final SOP crystals.

The production of crystalline fertilizers can be a complex endeavor. That makes proper screening and evaluation to identify the best process option – one that is able to deliver the desired quality and solubility – essential. Fertilizer producers therefore need to choose technology and equipment providers with proven expertise in both process development and commercial scale-up. Only providers that combine hands-on laboratory know-how with relevant industrial experience have the capability to build on their previous crystallization project successes and reproduce them reliably and consistently.

Veolia helps fertilizer producers position themselves in the specialty fertilizer market by diversifying their portfolios and lowering their reliance on traditional commodity products. Forward-looking producers can now seize higher-margin opportunities in the fast-growing horticultural market by producing – thanks to Veolia’s leading-edge HPD® crystallization technologies – specialty products both profitably and sustainably.

Originally published in Fertilizer International, July-August 2020